For the best part of the last two decades the "big 4" — made up of EY, Deloitte, PwC and KPMG — have dominated the world of professional services. Do business, or even just look at the accounts of, any major multinational company and you're likely to cross paths with the work of one of the audit, advisory, consulting, corporate finance, legal or tax divisions of the big 4.

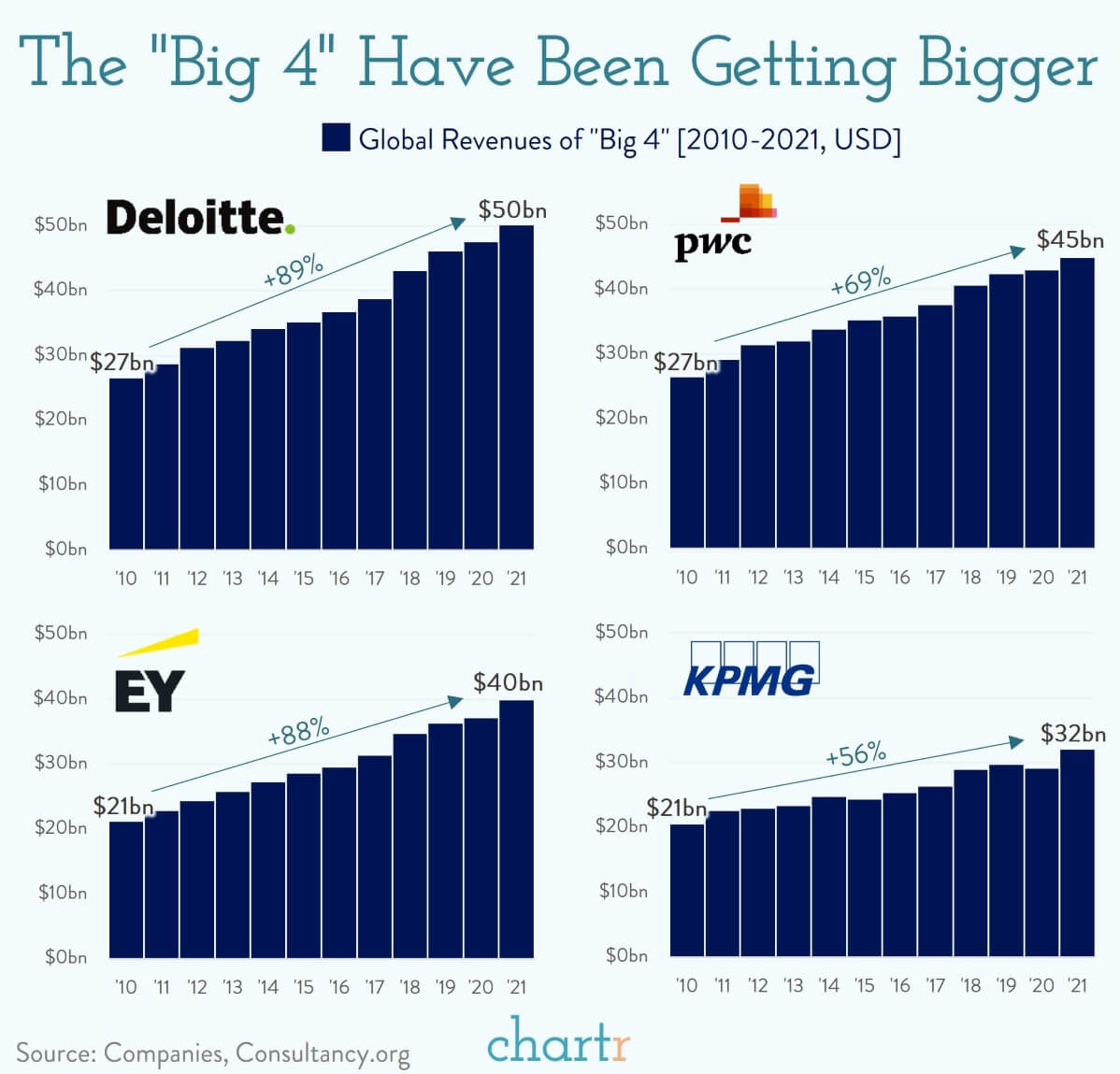

Indeed, in just over a decade the collective global revenue of the big 4 has risen from $95bn to $167bn. Deloitte, which is the biggest of the four, has also been the fastest growing — topping $50bn in revenue last year for the first time (that's more than Netflix, Twitter and Airbnb combined).

Breaking up the big 4?

Regulators have worried that the big 4 have gotten too big in the last 20 years. Together they audit pretty much every single major public company in America, and much of the western world, and conflicts of interest between the different services offered have been common.

So it was big news when EY announced recently that it was looking at splitting up its advisory and audit operations, which would be the biggest shake-up since the big 5 became the big 4 back during the collapse of Enron in 2002.

The thinking is that the EY consulting, and other non-audit teams, would be free to go after more clients, without having to worry about things looking fishy if EY also happens to be auditing the books. In recent years, all the extra services (non-audit) have been the source of growth, while audit has been a relative source of pain amidst recent major accounting scandals at Wirecard and Luckin Coffee. So far, EY's rivals have suggested they won't be looking at doing the same.